Customer Snapshot: Planning for the Future Through Remortgage

Meet Alex, a salaried professional in their early 40s based in the UK, with a stable job held for over seven years. With just a single dependent and no existing debt apart from a mortgage, Alex is in a strong financial position. Contemplating the next step, Alex sought guidance on remortgage options to raise equity for a buy-to-let investment property.

The Challenge: Releasing Equity to Invest Without Unnecessary Penalties

Alex’s goal was to raise approximately £60,000 from the equity in their existing home to fund a new investment property. However, there were several concerns:

- How much could be released without triggering early repayment charges (ERC) from an existing fixed-rate mortgage?

- Uncertainty about the best rate—whether to opt for a 2-year or 5-year fixed plan.

- Lack of clarity on monthly costs, documentation requirements, and product types when investing via personal name versus a limited company.

- Deciding if this financial move was a wise choice given market fluctuations.

Alex was looking for a clear, risk-free way to access funds, maximize potential returns, and keep options open as the property search continued.

The Solution: Tailored Remortgage for Investment Flexibility

After a detailed consultation, our advisor at Deal Direct provided Alex with a comprehensive breakdown, including:

- Timing the Remortgage: To avoid early repayment penalties, the new mortgage would commence once the current product expired, ensuring a seamless transition and saving potentially thousands in fees.

- Maximum Release Calculated: With a property value around £190,000 and just £60,000 owed, Alex could safely release up to £60,000, doubling their mortgage amount to a total of £120,000*

- Product Options Provided: Comparable monthly payments were modeled for both 2-year and 5-year fixed rates (between £730–£750/month at around 4% APR, based on a 20-year term), keeping repayment affordable and offering the flexibility to reassess as the market evolves.

- Guidance on Documentation: A step-by-step email was promised, listing all needed documents (passport, driver’s license, payslip, etc.) to streamline the application process.

- Investment Readiness: Clear advice was given on future options: once Alex found a property, further discussions could clarify the difference between remortgaging under a personal name versus forming a limited company for buy-to-let purposes.

*Precise figures subject to lender criteria and up-to-date valuations.

Results: Financial Clarity, No Penalties, and Investment Readiness

- No Early Repayment Charges: By timing the remortgage after the fixed period, Alex avoided unnecessary fees.

- Investment Ready: Funds can be released and ready to invest as soon as a suitable buy-to-let property is found.

- Clear, Predictable Payments: Monthly remortgage costs were laid out with multiple product options, giving Alex confidence to plan ahead.

- Expert Support: Ongoing guidance means Alex can return any time to revisit or fine-tune their remortgage or buy-to-let strategy.

“I don’t know what I’m doing, to be honest… but your breakdown really helped me see the options and costs. I can go away now, think things over, and come back ready to act.”

Answering Your Remortgage Questions

- How much equity can I release with a remortgage?

It depends on your current mortgage balance, property value, lender criteria, and affordability. In Alex’s case, around £60,000 was possible. - Can I remortgage without early repayment penalties?

Yes, timing is key. Wait until your fixed-rate period ends before remortgaging to avoid charges. - What documents are needed for a remortgage?

You’ll need ID (passport, driver’s license), recent payslips, and potentially details of the property to be purchased or the loan’s purpose. - Can I remortgage to fund a buy-to-let investment?

Yes, you can. If you plan to buy as a personal investor or through a company, different products and criteria will apply—our advisors can guide you. - Should I choose a 2-year or 5-year fixed rate?

Both have pros and cons. Shorter fixes offer flexibility if rates fall, while longer fixes offer stability. We model both options so you can decide what’s best.

Take the Next Step: Speak to a Remortgage Specialist

If you’re thinking about releasing equity through a remortgage – whether for investment, debt consolidation, or other needs – get tailored guidance from experts you can trust. Contact us today to discover the best rates, avoid penalties, and move towards your financial goals with confidence.

Ready to apply or see your best options?

Find your best deals online in minutes or request a no-obligation callback from one of our expert advisors to talk through your options or just get honest advice.

Related articles...

BTL Remortgage for Airbnb 2025 – Cornwall Success Story

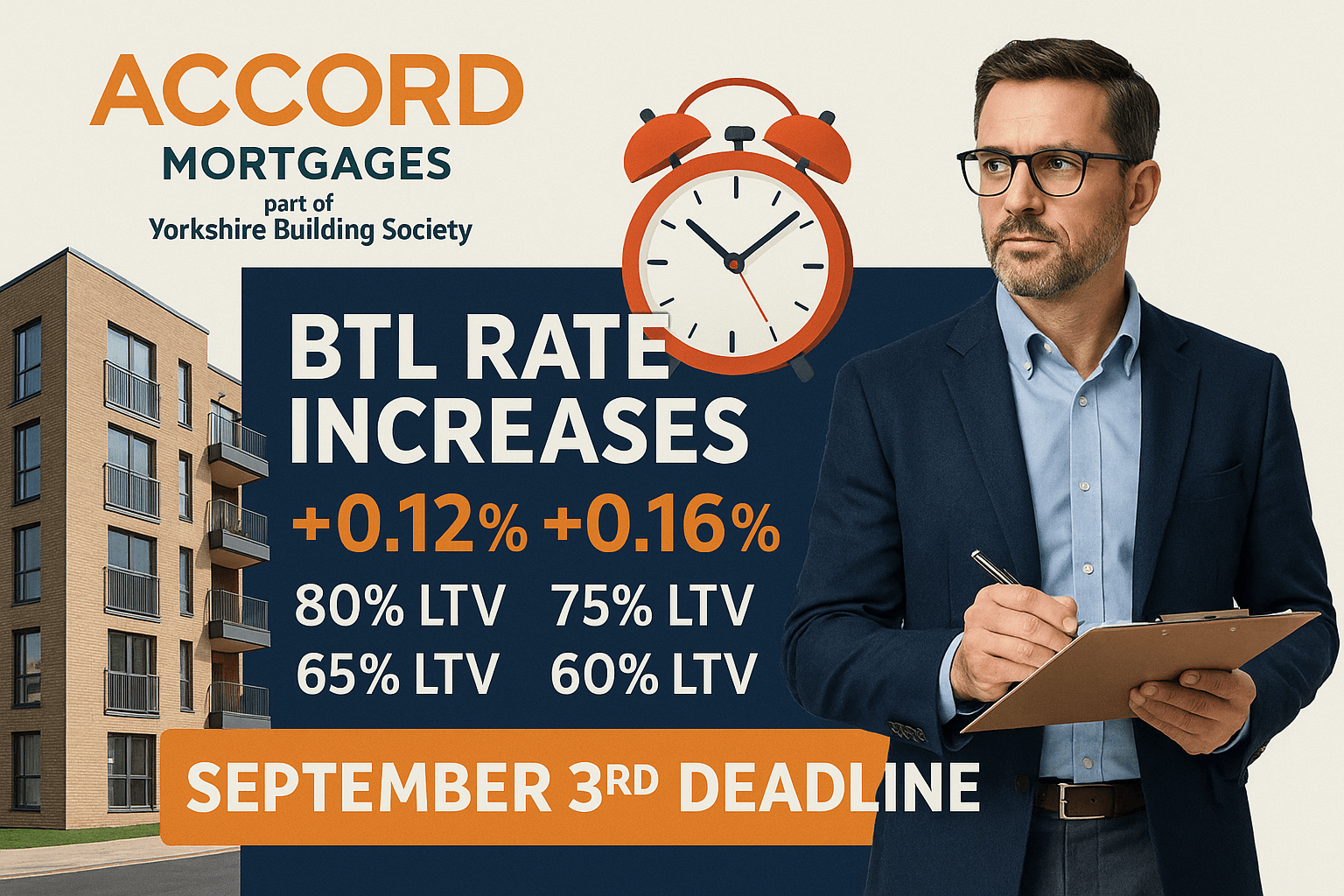

Accord Mortgages BTL Rate Rise Sept 2025 – Act by 3rd

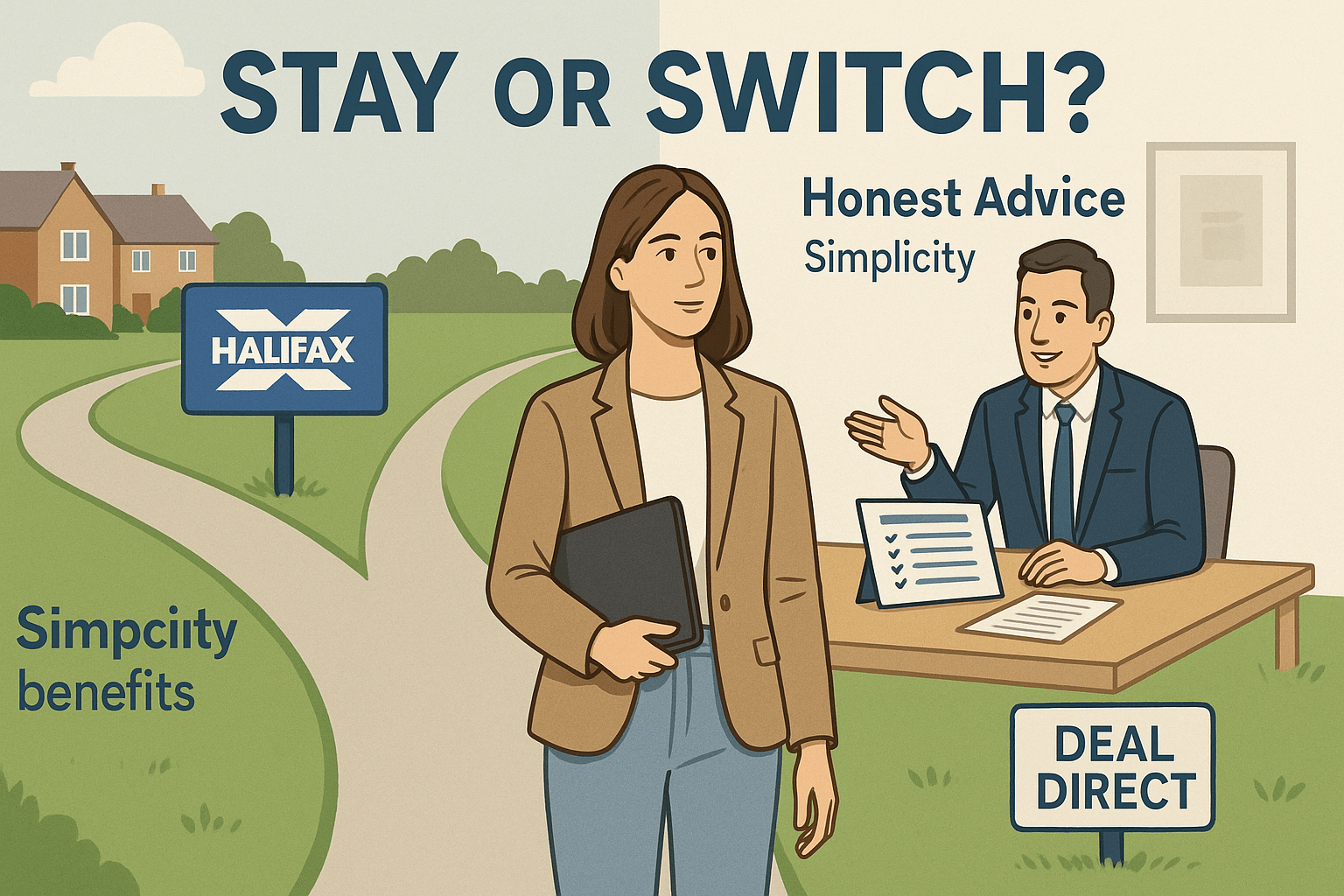

Stay or Switch Remortgage 2025? Halifax Case Study & Advice

As seen in...

Written by

| Senior Mortgage Adviser