Remortgage Rates UK: Halifax Cuts Rates August 2025

These changes include reductions to selected remortgage rates, updated product deadlines, and extended...

Read more

95% LTV Mortgages: Virgin Money Rate Hike Details for UK Buyers

This update is especially relevant for first-time buyers and applicants...

Read more

Accord Mortgages Cuts BTL & Residential Product Transfer Rates – August 2025 Update

If you are an existing Accord customer considering a switch or top-up...

Read more

Halifax Intermediaries Cut Fixed Rates for First-Time Buyers & Movers – July 2025 Update

Designed for both home movers and...

Read more

Santander Adjusts Fixed Mortgage Rates – Increases for High LTVs, Reductions for Remortgages & BTL

Santander has announced a new...

Read more

Leek Building Society Launches 2 Year Fixed Interest Only Mortgage – 2025 Update

Leek Building Society has introduced a new 2 year fixed rate Interest Only...

Read more

Barclays Updates Mortgage Rates & Reward Deals – July 2025 Product Changes Explained

These updates impact Barclays’...

Read more

NatWest Cuts Mortgage Rates & Increases Remortgage Cashback – July 2025 Update

These updates include rate reductions across several products, extended...

Read more

Leeds Building Society Cuts Buy to Let Rates – July 2025

Leeds Building Society has announced a series of updates including reduced interest rates...

Read more

TSB Cuts Mortgage Rates by Up to 0.30% for Existing Customers

TSB has announced a reduction in mortgage rates for existing...

Read more

What Mortgage Can I Afford? – Stop Guessing, Start Knowing

Most property buyers guess their mortgage affordability using outdated rules of thumb or basic online...

Read more

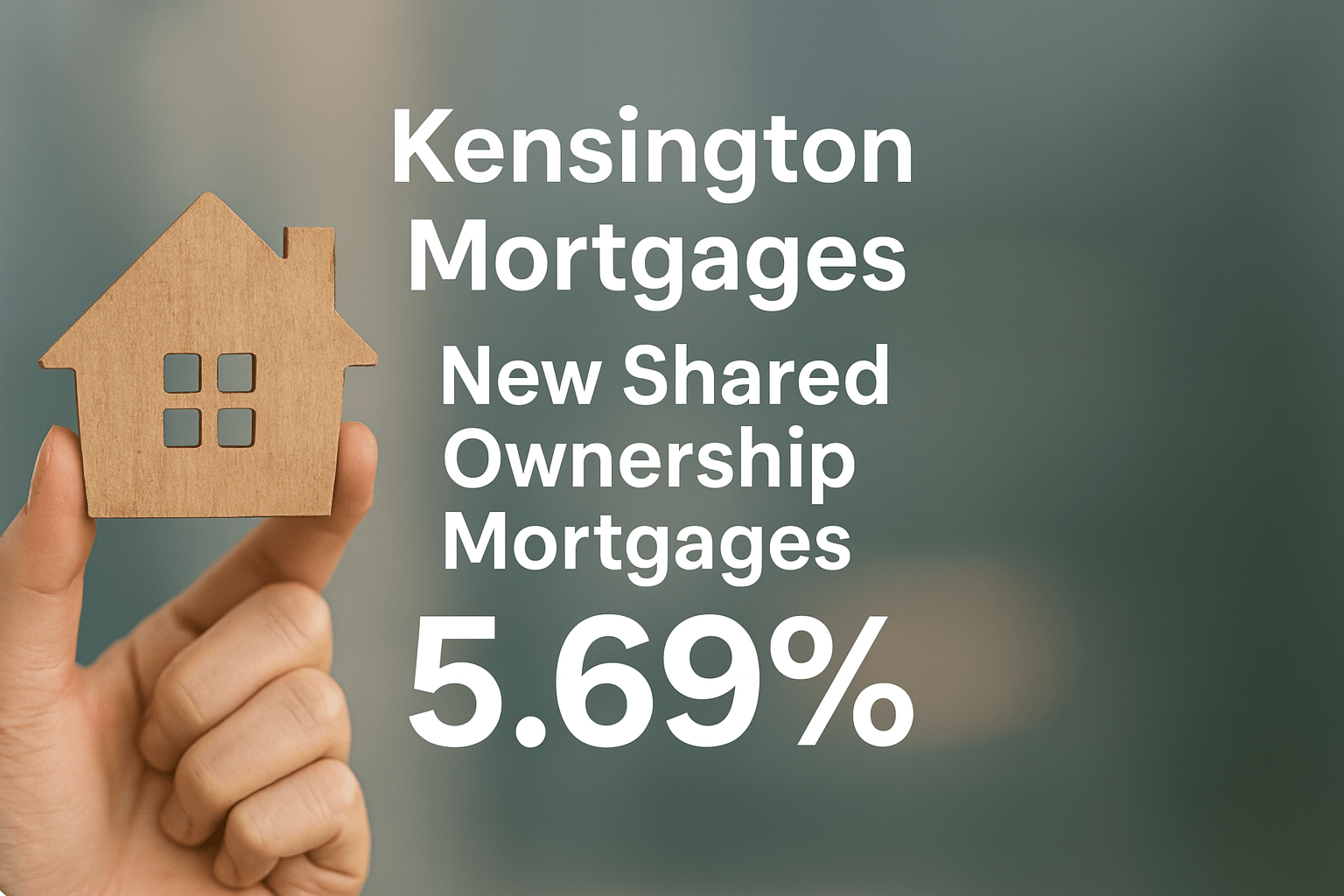

Kensington 95% LTV Shared Ownership Mortgages

Kensington Mortgages has announced significant rate reductions for Shared Ownership...

Read more

experience a 5 star customer service