Customer Overview

A homeowner in his mid-40s, working in a skilled trade and living in the Midlands, found himself overwhelmed by rising monthly expenses. With more money going out than coming in, he struggled to keep up with multiple debt repayments—including high-interest credit cards and a secured loan. Considering a debt consolidation remortgage could address these issues.

The Financial Challenge

Like many UK homeowners, this individual had accumulated debt due to unforeseen home and vehicle repairs. The debts included:

- High-interest credit card debt totalling over £14,000

- An existing secured loan of £29,675

- Total combined debts: £42,340

Despite maintaining repayment discipline, the juggling act between bills, debts, and essentials left little room for error or savings. He had no emergency fund and relied heavily on credit cards for unexpected expenses. His primary goal: consolidate debt and reduce financial pressure while creating room to save.

The Remortgage Solution

After a detailed consultation, the customer was advised to remortgage and consolidate his debts into his mortgage. This approach offered the following benefits:

- Combining his mortgage, secured loan, and credit card debts into one manageable monthly payment

- Extending the mortgage term to spread repayments more affordably

- A lower overall monthly commitment by blending high-interest loans into a lower-interest mortgage

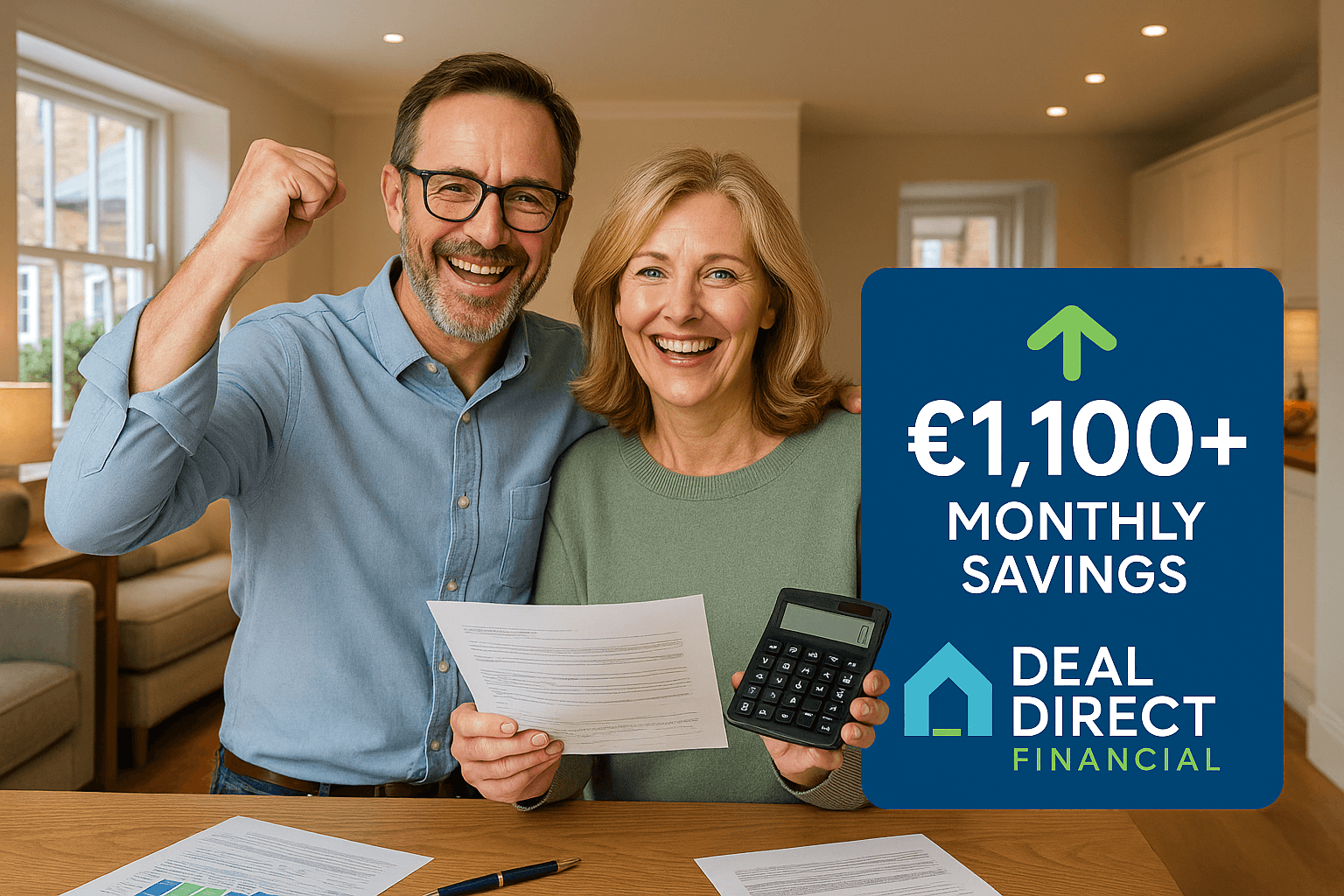

While consolidating debt into a longer-term mortgage increases the overall interest paid—approximately £69,861 over the loan term—it created short-term relief and long-term stability. The remortgage helped reduce his outgoing debt payments by £271.68 each month, freeing up cash for savings and everyday living costs. Choosing the right debt consolidation remortgage strategy was crucial for these outcomes.

Immediate Results and Long-Term Benefits

- Monthly disposable income increased by £271.68

- Debt stress eliminated; all high-interest obligations consolidated into one manageable payment

- Total savings of £3,861 over the loan term estimated if only minimum repayments had been maintained on original credit debts

- Improved financial control and capacity to build an emergency savings fund

“It was getting harder each month to just keep my head above water. Now, I finally have room to breathe and can start saving properly. It feels like I’m in control again.” – Anonymous Homeowner

Understanding the Reason Behind the Debt

The homeowner’s financial difficulty stemmed from essential expenses, including emergency car repairs, water damage under flooring, and urgent home repairs like a broken shower and dishwasher. These unexpected costs forced him to rely on credit. This remortgage solution enables him to avoid such reliance on credit in the future by setting aside monthly savings for emergencies. The implementation of a debt consolidation remortgage ensures a more secure financial future.

Why a Full Debt Consolidation Remortgage Was the Right Choice

After reviewing partial versus full consolidation, it was clear that consolidating all debts into the mortgage created the most financial breathing room. While he kept one small credit card to manage separately, the majority of burdensome payments were eliminated, offering faster relief through a full debt consolidation remortgage.

FAQ: Debt Consolidation Remortgage Explained

How much can I save monthly by consolidating credit card debts into a mortgage?

In this case, the customer saved approximately £271.68 per month. Actual savings depend on your total debts, interest rates, and new mortgage terms.

Can you remortgage to pay for emergency repairs or car upgrades?

Yes. Beyond consolidating debts, the customer also used part of the remortgage to upgrade his vehicle and create a savings buffer for future repairs.

Does remortgaging affect my credit score?

Initially, remortgaging can affect your credit score due to the credit checks involved. Over time, consistently making payments on the new mortgage can improve your credit profile, which can be a positive effect of a debt consolidation remortgage.

What documents are required for a remortgage application?

- Current mortgage details

- ID and proof of address

- Recent bank statements

- Proof of income (e.g. payslips or self-employment income)

- Details of existing debts integrated into a debt consolidation remortgage

Can I repay a fixed-rate mortgage early without penalties?

This depends on the lender’s terms. Many fixed-rate mortgages include Early Repayment Charges (ERCs), so it’s important to check your Key Facts Illustration (KFI) or speak with your broker before proceeding.

Start Your Journey Toward Financial Freedom

If you’re struggling with multiple debts and looking to reduce your monthly outgoings, a debt consolidation remortgage may be the right solution. Speak with our specialist brokers today to explore tailored options and take the first step toward long-term financial control.

Ready to see how much you could save? Use our remortgage calculator or contact us now for a free consultation.

Ready to apply or see your best options?

Find your best deals online in minutes or request a no-obligation callback from one of our expert advisors to talk through your options or just get honest advice.

Related articles...

Debt Consolidation Remortgage: Save £1,383/Month in 2025

Debt Consolidation Remortgage for Financial Relief

Debt Consolidation Remortgage Case Study – Pepper Money 2025

As seen in...

Written by

| Mortgage Advisor