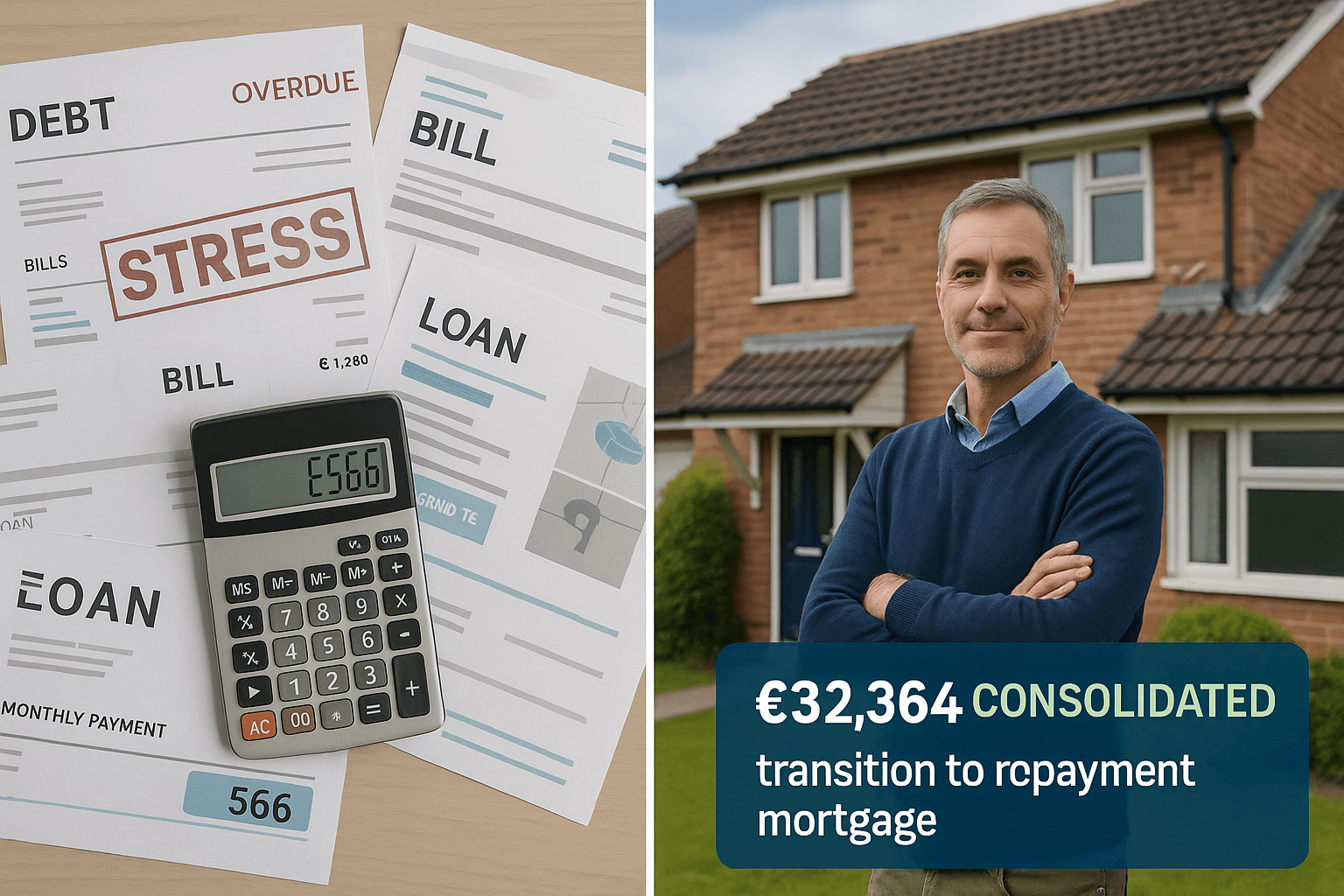

Overview: Debt Consolidation Through Remortgage

A 40-something homeowner from Northern England, working in a professional sector, recently opted for a debt consolidation mortgage to take control of their financial future. When they considered the services offered by Deal Direct, a particularly favorable debt consolidation remortgage deal caught their eye. They soon discovered that the Deal Direct debt consolidation remortgage was perfect for their needs. After years of investing in home improvements and facing some unexpected costs, they found themselves juggling multiple high-interest debts—from credit cards to car finance.

With their fixed mortgage rate nearing its end, they explored the opportunity to remortgage and simplify their financial commitments. The result? Substantial monthly savings and renewed financial flexibility through a Deal Direct offer.

The Financial Challenge

Home improvements had been a worthwhile investment, but costs overshot the original budget. To cover the shortfall, the homeowner relied on unsecured borrowing—including:

- High-interest credit cards (up to 35%)

- Car loans with high monthly payments

- Hire Purchase agreements

Despite managing repayments responsibly, the total debt climbed to over £22,377.40. Monthly payments toward these debts totalled about £551, putting pressure on their disposable income.

With no savings to fall back on and a desire to avoid future financial strain, they wanted a long-term solution: one affordable monthly payment, less stress, and more stability, leading them to consider Deal Direct’s debt consolidation remortgage options.

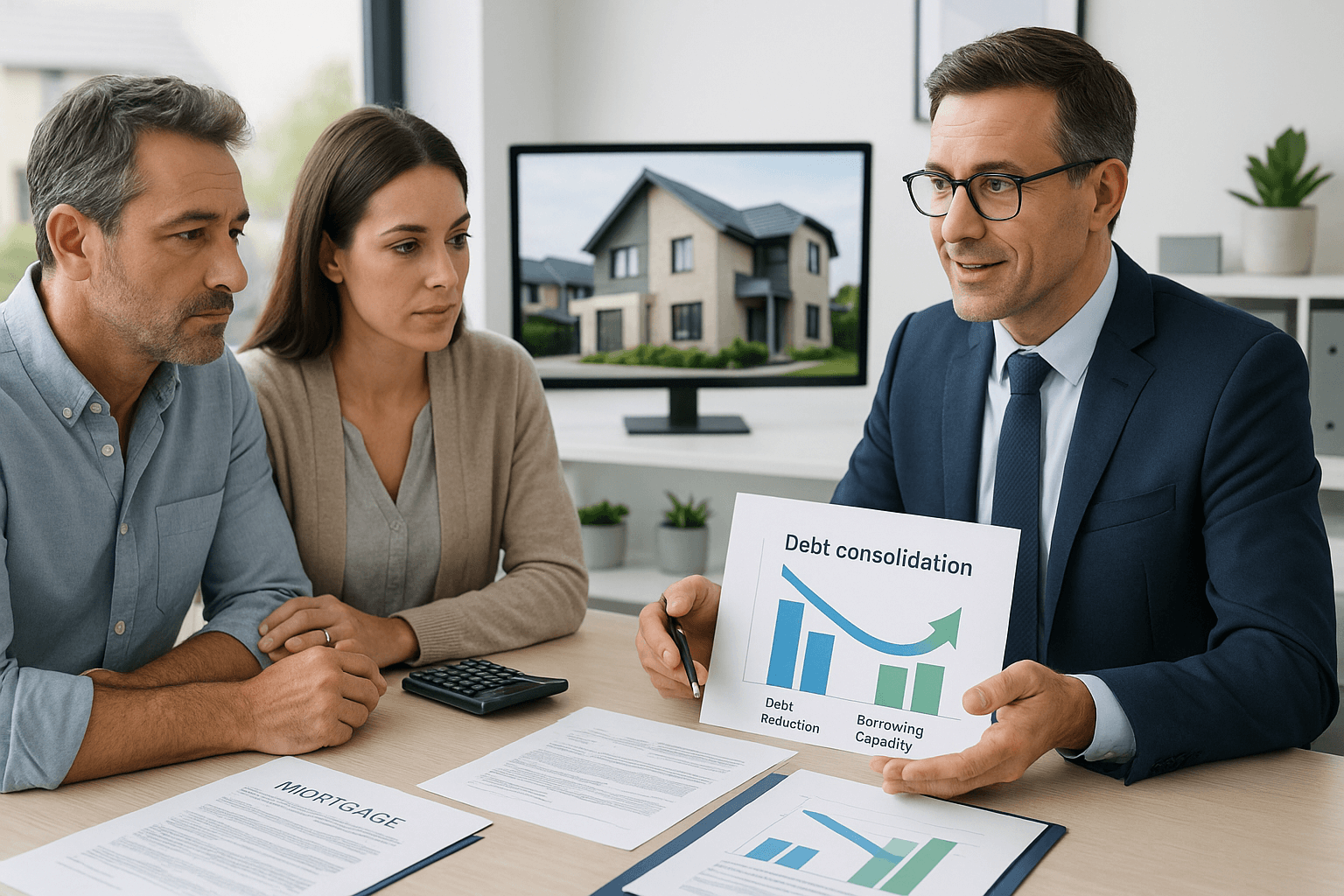

The Solution: Debt Consolidation Remortgage

Our mortgage specialists identified a suitable debt consolidation remortgage plan that would allow the client to roll key debts into their mortgage. This meant exchanging multiple high-cost commitments for one manageable repayment, taking advantage of lower mortgage interest rates.

As part of the remortgage, the following debts were consolidated:

- Credit cards with high interest (up to 35%)

- Two car finance agreements with substantial monthly payments

By selecting only the highest-cost debts—and leaving low or zero-interest debts out of the mortgage—the client avoided unnecessary borrowing. This measured approach ensured the new mortgage balance remained as low as possible.

We advised on the long-term cost implications, including the fact that consolidating debt into a mortgage would mean paying it over a longer period. However, the client prioritised monthly affordability and financial stability, appreciating Deal Direct’s intervention.

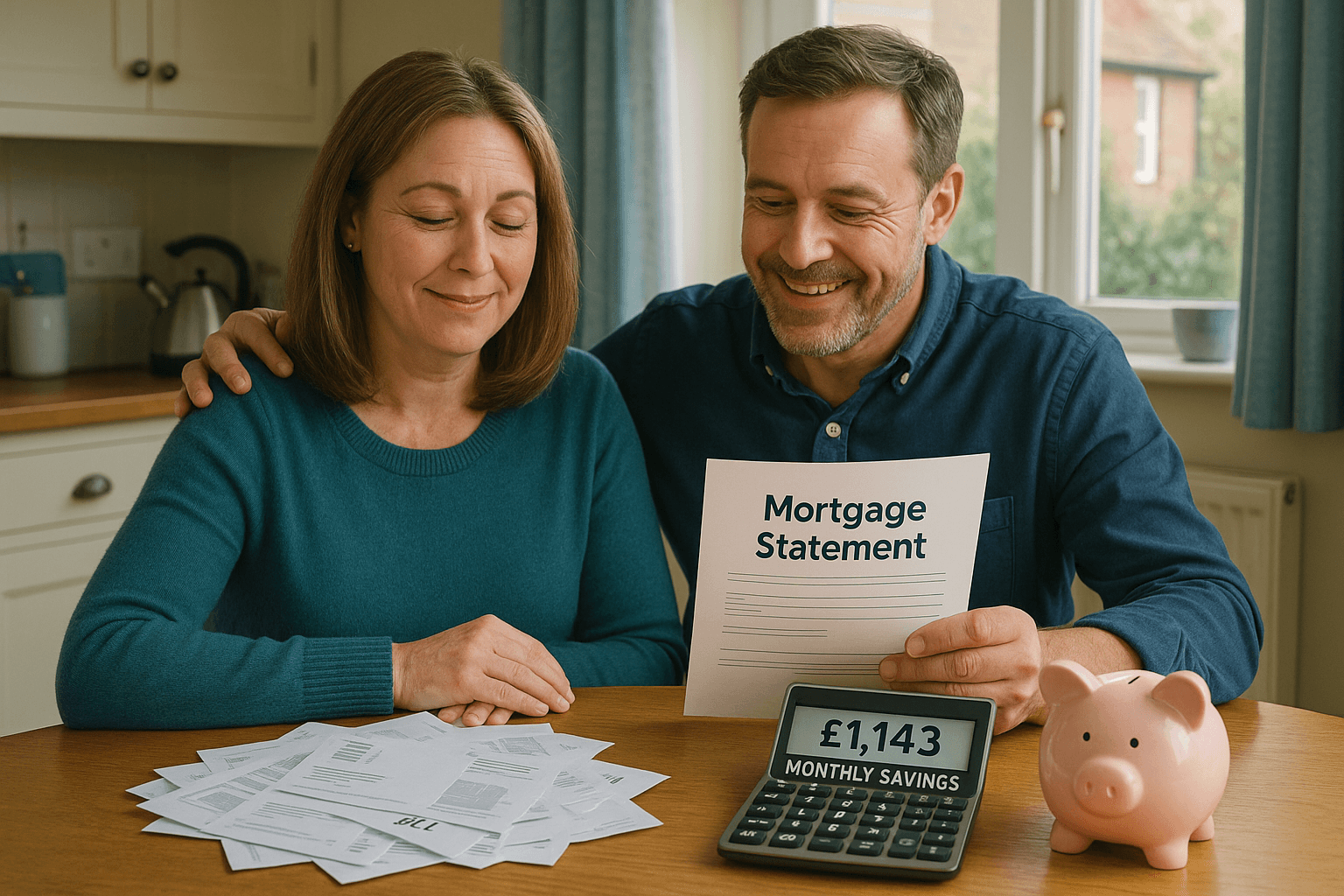

Results Achieved

The remortgage provided significant benefits:

- Monthly savings of approximately £490.58—freed up by replacing multiple payments with a single, lower mortgage repayment.

- Simplified finances, making it easier to manage household budgeting.

- Stabilized their credit profile by reducing the risk of missed payments.

- Enabled the client to start building savings again and even plan mortgage overpayments.

While the long-term total cost of the consolidated debts will amount to around £47,216.31, this was a known and accepted trade-off in exchange for improved monthly cash flow and financial breathing space through the Deal Direct remortgage.

“The home improvements are done, and now it’s time to get our finances in order. With this remortgage, we’re finally in a position to save again. We’ve reduced our monthly outgoings and can focus on building our financial future without stress.”

Frequently Asked Questions

How much can I save monthly by consolidating credit card debts into a mortgage?

In this case, the homeowner saved nearly £490 per month. Monthly savings vary based on your existing debts, interest rates, and the new mortgage deal you’re eligible for.

Can you remortgage to fund home improvements?

Yes. Many homeowners choose to remortgage to raise capital for renovations. In this instance, previous home improvement borrowing led to unsecured debt, which was consolidated during the remortgage.

Does remortgaging affect my credit score?

Remortgaging itself does not significantly affect your credit score, but a hard credit check and changes in credit utilisation may have a temporary impact. In the long term, consolidating debts and maintaining payment discipline can improve your credit standing.

What documents are required for a remortgage application?

Commonly required documents include proof of identity, proof of income (e.g., payslips, P60), bank statements, existing mortgage details, and information about your debts (loan statements, credit card balances).

Can I repay a fixed-rate mortgage early without penalties?

Early repayment charges may apply during the fixed-rate term. Once the term ends, most lenders allow penalty-free overpayments. It’s crucial to review your mortgage agreement or ask your advisor for clarity.

Take Control of Your Finances Today

If you’re struggling with multiple debts or just want to simplify your finances, a remortgage to consolidate debt could be the right step. Let our expert mortgage advisors guide you through the process—ensuring you understand the costs, benefits, and best options for your situation.

Contact us today to discuss your remortgage options and take the first step toward financial freedom.

Ready to apply or see your best options?

Find your best deals online in minutes or request a no-obligation callback from one of our expert advisors to talk through your options or just get honest advice.

Related articles...

Debt Consolidation Mortgage Case Study Success Story 2025

Debt Consolidation Mortgage: Boost BTL Borrowing Power 2025

Debt Consolidation Remortgage: Save £1,143 Monthly 2025

As seen in...

Written by

| Mortgage Advisor