Customer Overview: Assessing Options Before Remortgaging

A recent inquiry featured a homeowner in their early 40s, employed in the professional sector and residing in a suburban area of the UK. The customer reached out, initially expressing interest in exploring their mortgage options – particularly with regards to debt consolidation mortgages. However, their current mortgage deal still has approximately two years remaining, prompting them to investigate their choices well in advance.

Main Challenge: Should You Remortgage Now or Wait?

This homeowner’s main concern centered on whether it’s advisable to remortgage for debt consolidation now, or to wait until closer to the end of their current fixed-rate mortgage. They were especially interested in understanding the potential benefits and drawbacks, and what alternatives might exist while their current mortgage remains active.

Exploring Debt Consolidation Remortgage Solutions

A debt consolidation mortgage allows homeowners to combine various unsecured debts – like credit cards and personal loans – into their mortgage by releasing equity. This can potentially lower monthly payments and simplify finances. The homeowner was right to seek information early; timelines and circumstances can significantly affect available deals and overall savings.

At Due Direct, our mortgage specialists review your current mortgage terms, outstanding debts, and long-term financial goals. We use tools such as a remortgage calculator to model possible interest savings and forecast new monthly payments. For property owners whose fixed mortgage terms have some time left, switching too early could incur early repayment penalties. However, some lenders offer deals with flexibility or with specially tailored products for debt consolidation needs.

- Comparisons of current and forecasted remortgage rates

- Assessment of early repayment charges

- Guidance on secured loan alternatives if remortgaging isn’t ideal yet

- Long-term planning advice to maximise future savings

Is It Worth Remortgaging Early?

In most cases, it’s best to wait until the last few months of your mortgage deal before remortgaging, especially when considering debt consolidation. Remortgaging too soon can lead to penalties that outweigh any benefits. Instead, pre-planning (just like this inquirer did) provides valuable insights and ensures you’re ready to act when the timing is right.

Results: Informed Decision-Making and Financial Peace of Mind

Although no immediate action was taken, the customer benefitted by confirming that exploring options was a wise step, even if only for future reference. Through this consultation, they learned:

- How far in advance they should start preparing for a debt consolidation remortgage

- The importance of tracking current mortgage end dates and penalty periods

- Alternative strategies (such as secured loans) available before remortgaging is viable

“I was just exploring the market really… it’s useful to know what I might be able to do when my current deal ends.”

Early engagement with a mortgage expert allowed the homeowner to gain clarity and prepare for a smarter financial transition when their current fixed rate comes to an end.

Frequently Asked Questions (FAQs)

- Q: Can you remortgage to consolidate debt before your current deal ends

A: You can, but be aware of potential early repayment penalties and higher costs. It’s usually more cost-effective to wait until your fixed rate or tied-in period is about to end. - Q: How early should I start looking at remortgage options?

A: Ideally, start researching deals and consulting with specialists about 6–12 months before your current deal expires. - Q: What if I have debts I want to consolidate now?

A: You could explore secured loans as an interim solution, but review terms carefully with a qualified advisor to avoid extra costs. - Q: Will looking into remortgaging affect my credit score?

A: Quotations and basic eligibility checks typically have no impact; only formal applications may result in a hard credit search. - Q: What documents will I need to prepare when applying for a remortgage?

A: Prepare copies of your current mortgage statement, proof of income (such as recent payslips), photo ID, and evidence of any debts you wish to consolidate.

Ready to Explore Your Remortgage Options?

Whether you plan to act now or in the future, it pays to understand your options. Speak to one of our mortgage specialists today to get your personalized debt consolidation mortgage plan – and be ready when the timing is right!

Ready to apply or see your best options?

Find your best deals online in minutes or request a no-obligation callback from one of our expert advisors to talk through your options or just get honest advice.

Related articles...

BTL Remortgage for Airbnb 2025 – Cornwall Success Story

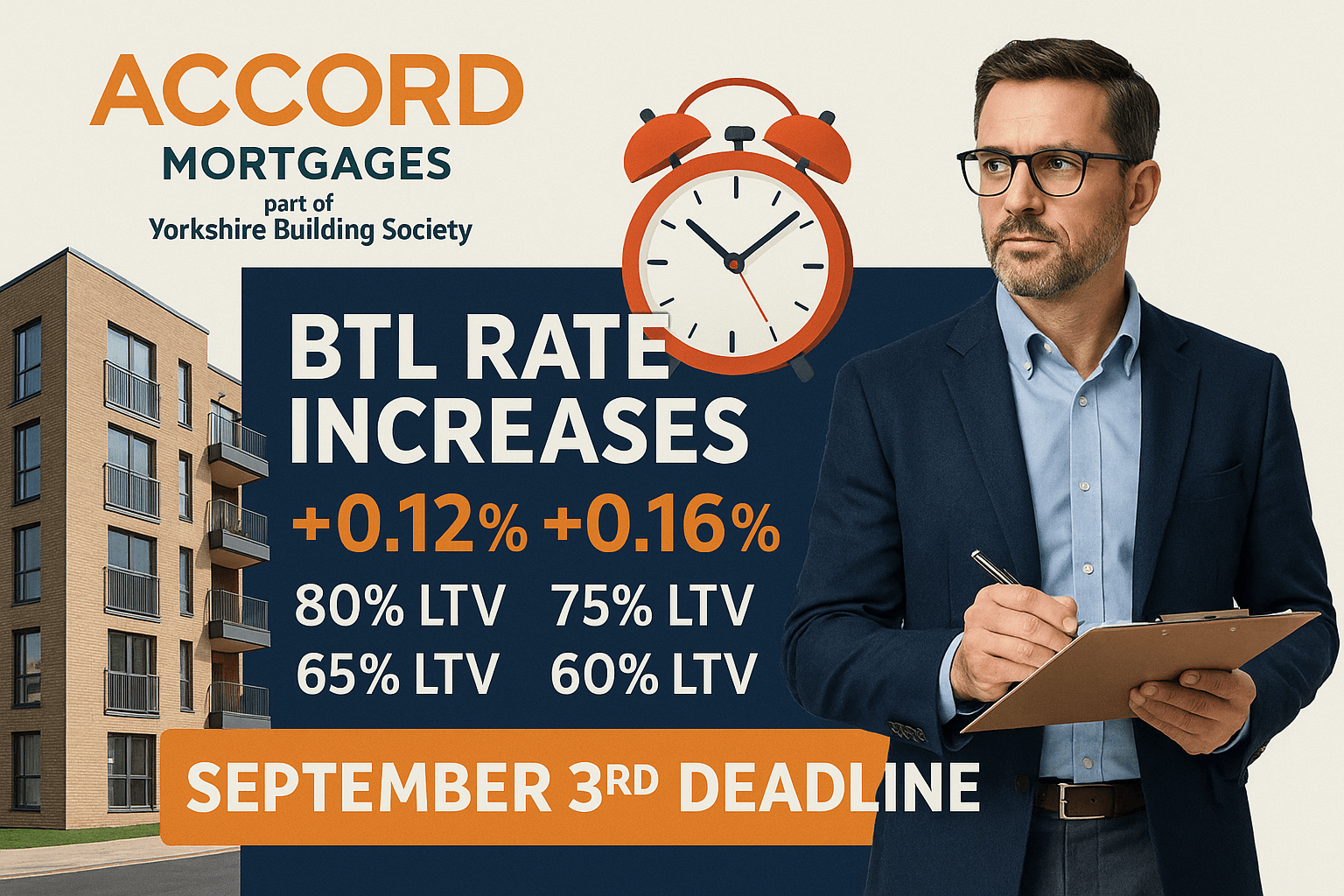

Accord Mortgages BTL Rate Rise Sept 2025 – Act by 3rd

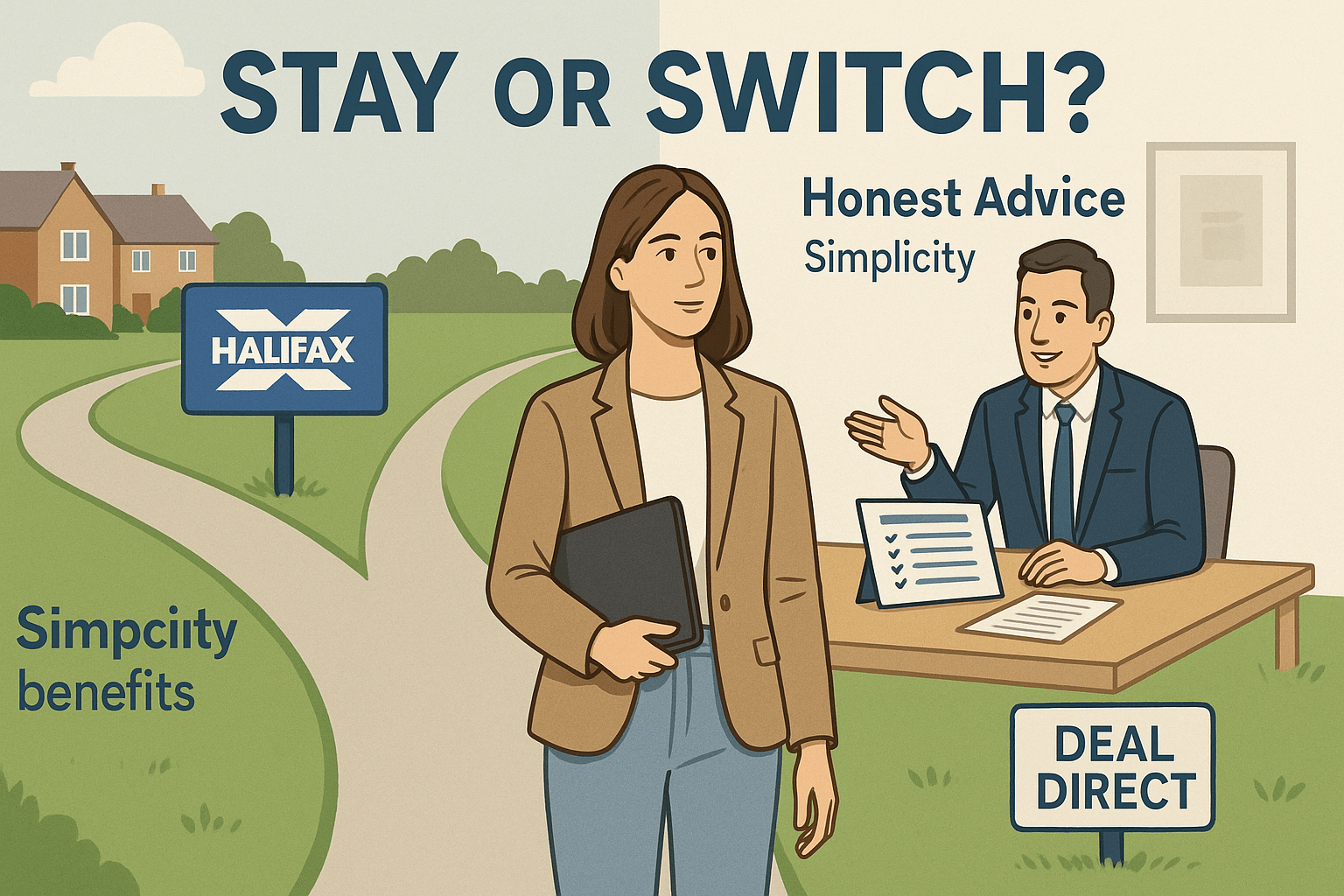

Stay or Switch Remortgage 2025? Halifax Case Study & Advice

As seen in...

Written by

| Mortgage Advisor