Significant Lending Criteria Changes Announced by Tandem Bank

Tandem Bank, a leading UK mortgage lender, has unveiled substantial improvements to its mortgage lending criteria and product packaging. These updates deliver greater flexibility, especially benefiting homebuyers, property investors, and self-employed applicants across the UK.

This article provides a straightforward overview of the key changes and what they mean for those seeking a new mortgage, a remortgage, or looking to expand their property portfolio in 2025.

Summary of Key Mortgage Criteria & Policy Changes

- 1st Mortgage Consent Eased: No consent required where a restriction by the first mortgagee appears on the Land Registry (certain obligations to lend remain). The previous condition requiring the Land Registry to be updated for loans over £100,000 has been removed.

- Occupiers Waiver Streamlined: Except in the case of married applicants borrowing in sole name, occupiers’ waivers are no longer routinely required for residents aged 17+.

- Improved AVM (Automated Valuation Model) Limits: For applications with loan-to-value (LTV) of 50% and below, the required Confidence Level has been reduced to 4.0.

- Substantial Increases to Maximum Advance & LTV: Borrowers can access higher loan amounts and LTV bands—improving affordability and flexibility.

- Simplified Self-Employed Requirements: Underwriting streamlined for limited company directors (over 25% shareholding), sole traders, and partners—fewer documents and clearer income calculation.

Who Benefits Most from Tandem’s Criteria Updates?

- Self-employed borrowers seeking clearer and more accessible underwriting.

- Remortgage applicants and those with complex property ownership structures.

- Landlords and property investors looking to optimise LTV and borrowing capacity.

- Pipelined mortgage applications may retrospectively benefit from these improvements.

Detailed Overview of Tandem’s Product & Policy Adjustments

1st Mortgage Consent Policy

Tandem Bank now waives the consent requirement where a first mortgagee’s restriction is shown in the Land Registry. The previous policy mandating an up-to-date Land Registry entry for loans above £100,000 is also abolished. These changes streamline applications for buyers with complex security arrangements or layered charges—speeding up approval for many borrowers.

Changes to Occupiers Waiver/Disclaimer

For most applicants, especially where residents over 17 are involved, Tandem will generally not require occupiers’ waivers. The only exception is for married applicants in sole name. Applicants who are divorced or separated must continue to disclose status and may need to provide evidence (such as a Deed of Separation).

Updated AVM Limits for Low LTV Cases

For borrowers securing loans at 50% LTV or below, the required AVM Confidence Level is reduced to 4.0. This adjustment should make it easier for low-LTV applicants to proceed with automated property valuations, facilitating faster processing and decision-making.

Increased Maximum Loan & LTV Bands

- Higher loan amounts and LTV ratios are now available on Tandem’s product range for qualifying borrowers.

- These improvements can be applied to applications already in progress by re-scoring current cases.

If you are unsure how these improved maximums apply to you, reach out for a personalised review.

Simplified Income Verification for the Self-Employed

- Required documents: Last 2 years’ SA302s and Tax Year Overviews.

- If latest SA302 is over 9 months old: Provide 3 months’ business bank statements (covering last 60 days).

- Net monthly income is based on the latest year, unless significantly lower than the previous year.

- If income jumps by more than 30%, an explanation is needed (possibly via accountant).

- If income drops by 30%+ year-on-year, 3 months’ business bank statements required for trend assessment.

These updates mean faster, more predictable underwriting for self-employed applicants.

Why Choose Tandem Bank for Your Next Mortgage?

- Flexible criteria—ideal for complex property cases, investors, and the self-employed.

- Streamlined documentation for quicker, less stressful approval.

- Enhanced loan amounts and LTVs mean you can borrow more, even in challenging scenarios.

- Fast pipeline benefit: Existing applicants can take advantage of new terms quickly.

Whether you’re buying, remortgaging, consolidating debt, or taking advantage of home improvement opportunities, Tandem’s new criteria are designed to make borrowing simpler and more accessible in 2025.

Need Personalised Mortgage Advice?

Our expert team is ready to guide you through Tandem’s updated options—contact us today for a tailored assessment and to secure the best solution for your circumstances.

Frequently Asked Questions

- Who qualifies for Tandem’s enhanced mortgage criteria?

UK residential and buy-to-let borrowers, including self-employed applicants, those with complex ownership structures, and low-LTV borrowers may qualify under the revised criteria. - How do the AVM and LTV changes affect my mortgage application?

Lower AVM confidence levels and higher LTV caps can make loans faster to arrange and offer higher advances—contact us to see how this applies to your circumstances. - Is Tandem suitable for self-employed mortgage applicants?

Yes. Tandem’s streamlined income verification makes approvals easier and faster for limited company directors, sole traders, and partners. - How do I apply for a mortgage with Tandem or check my eligibility?

Contact our specialist team for a no-obligation consultation. We’ll assess your options based on Tandem’s updated criteria and guide you step-by-step. - What is the pipeline and rate validity period?

The current pipeline and rate validity window for Tandem mortgage applications is 30 days.

Ready to apply or see your best options?

Find your best deals online in minutes or request a no-obligation callback from one of our expert advisors to talk through your options or just get honest advice.

Related articles...

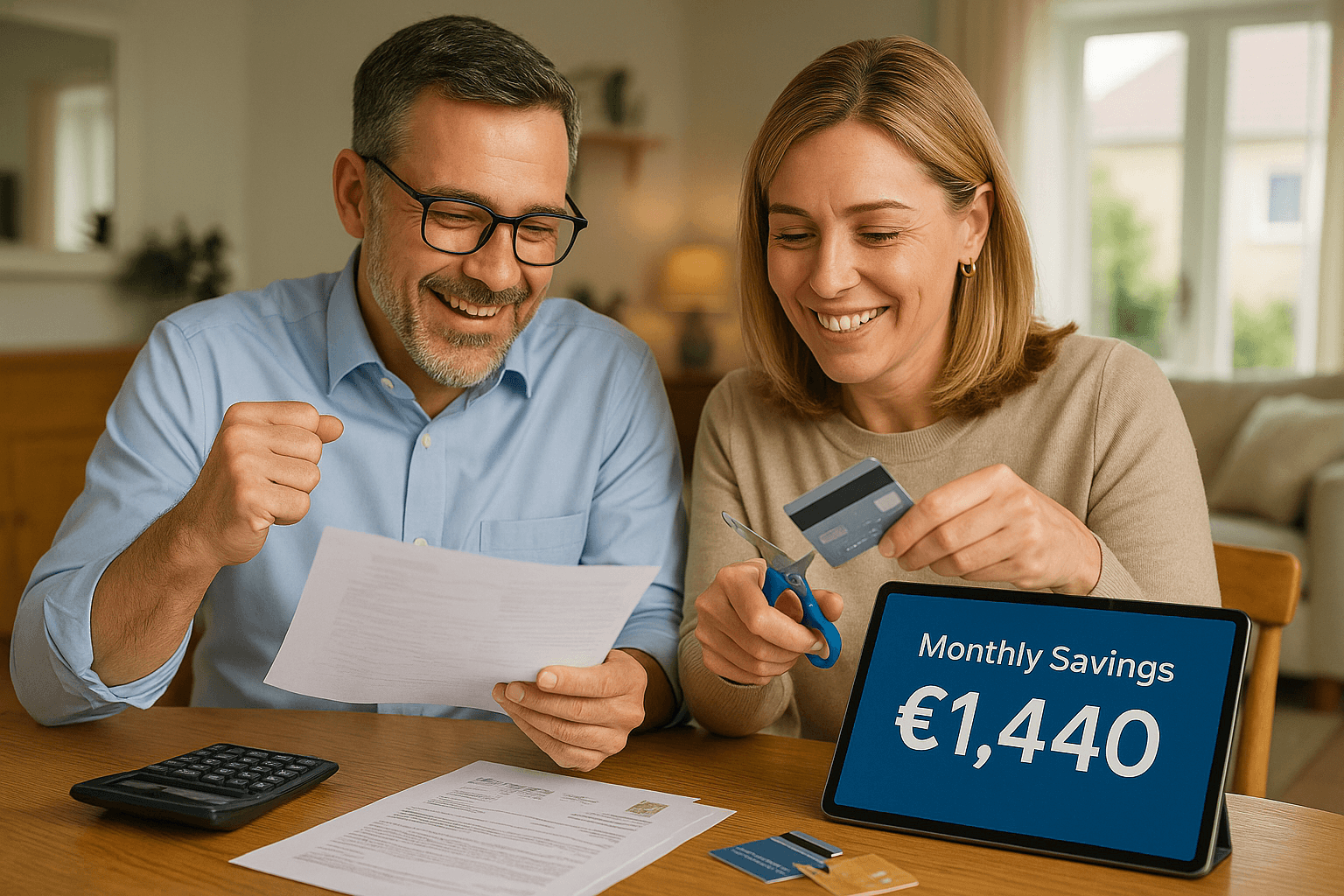

Debt Consolidation Remortgage Saves £1,440 Monthly

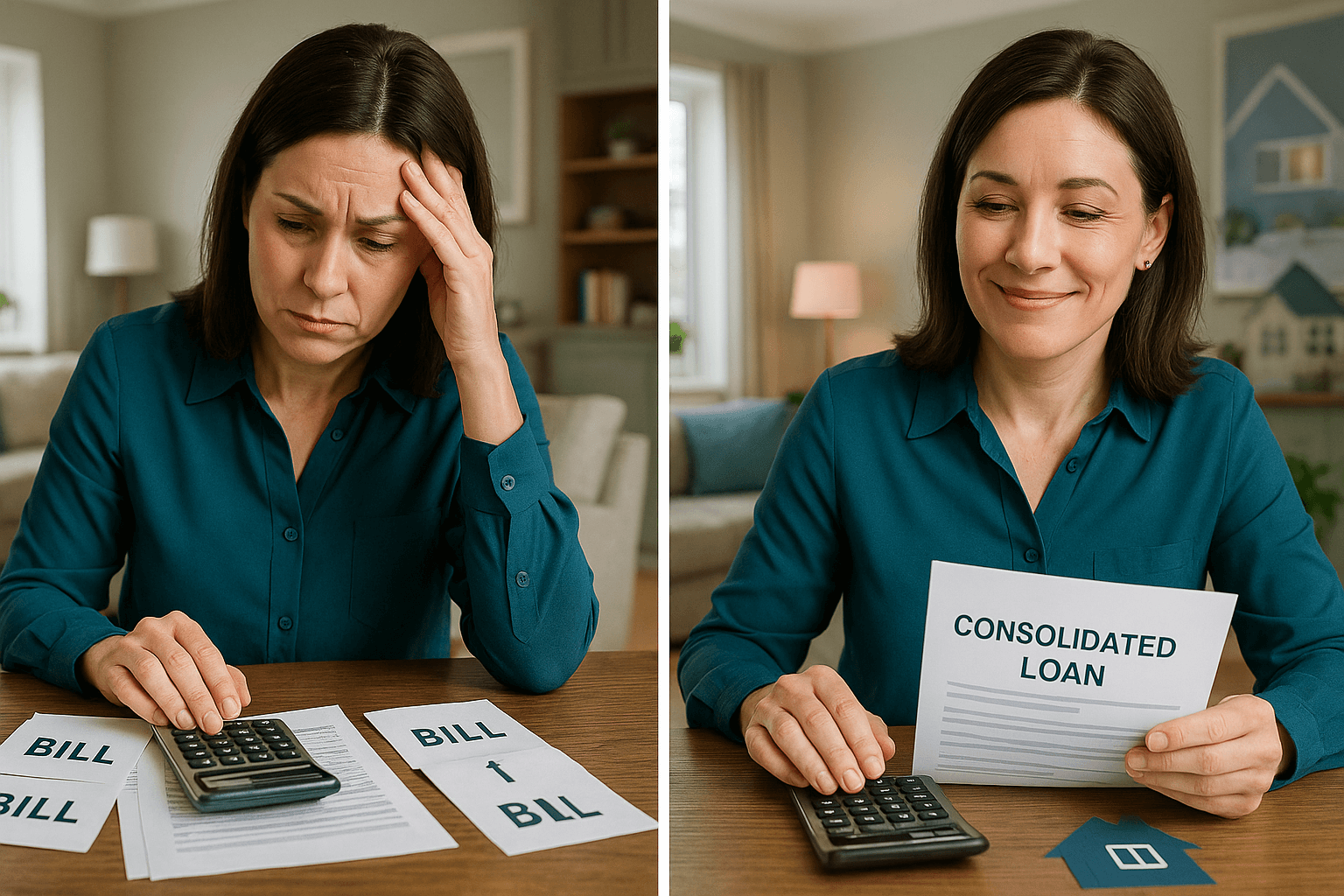

Debt Consolidation Remortgage Case Study 2024 – £1085 Saved

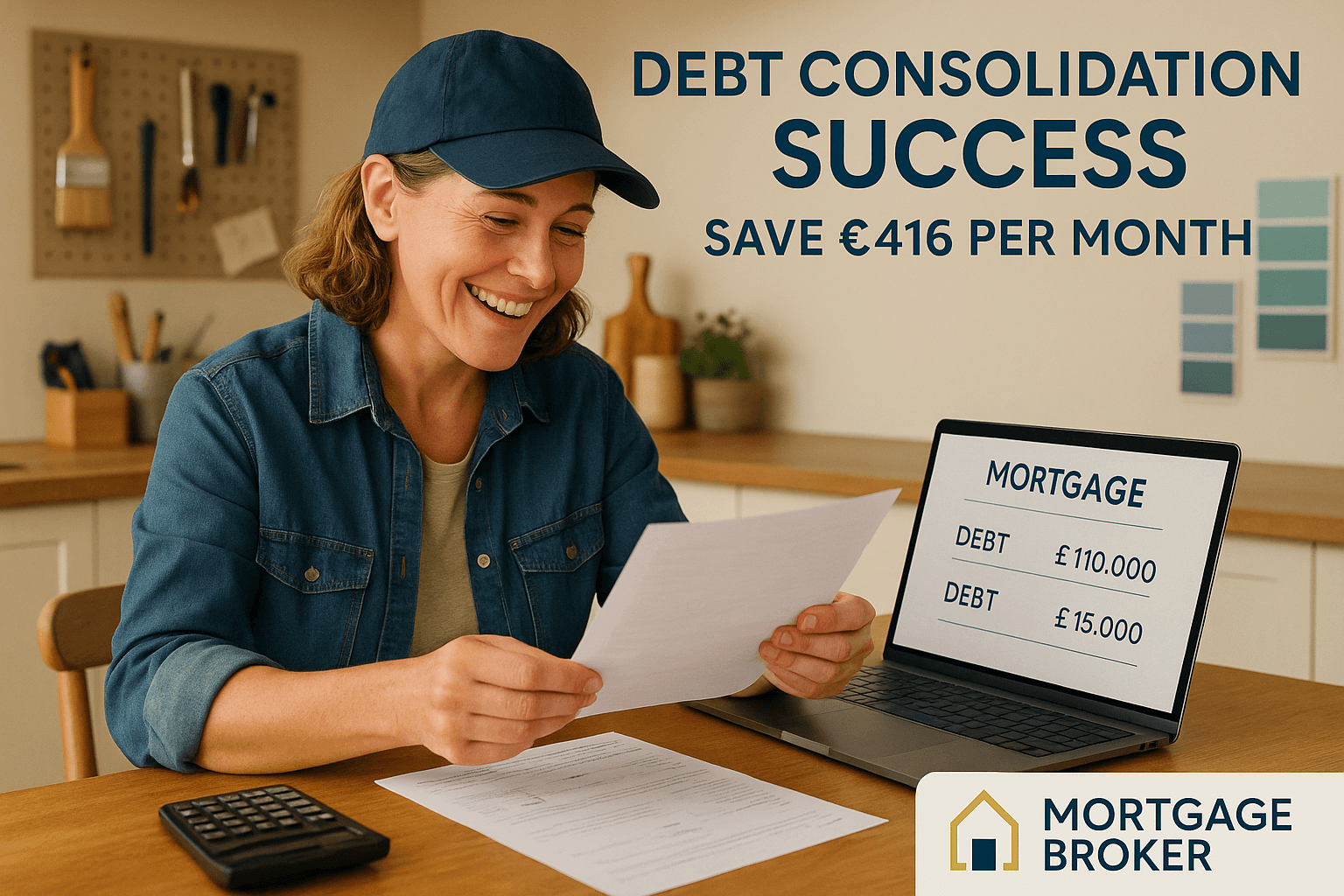

Debt Consolidation Mortgage Saves £416 Monthly – Case Study

As seen in...

Written by

| Mortgage Advisor